Empowering consumers to end the cycle of financial stress

0 min read

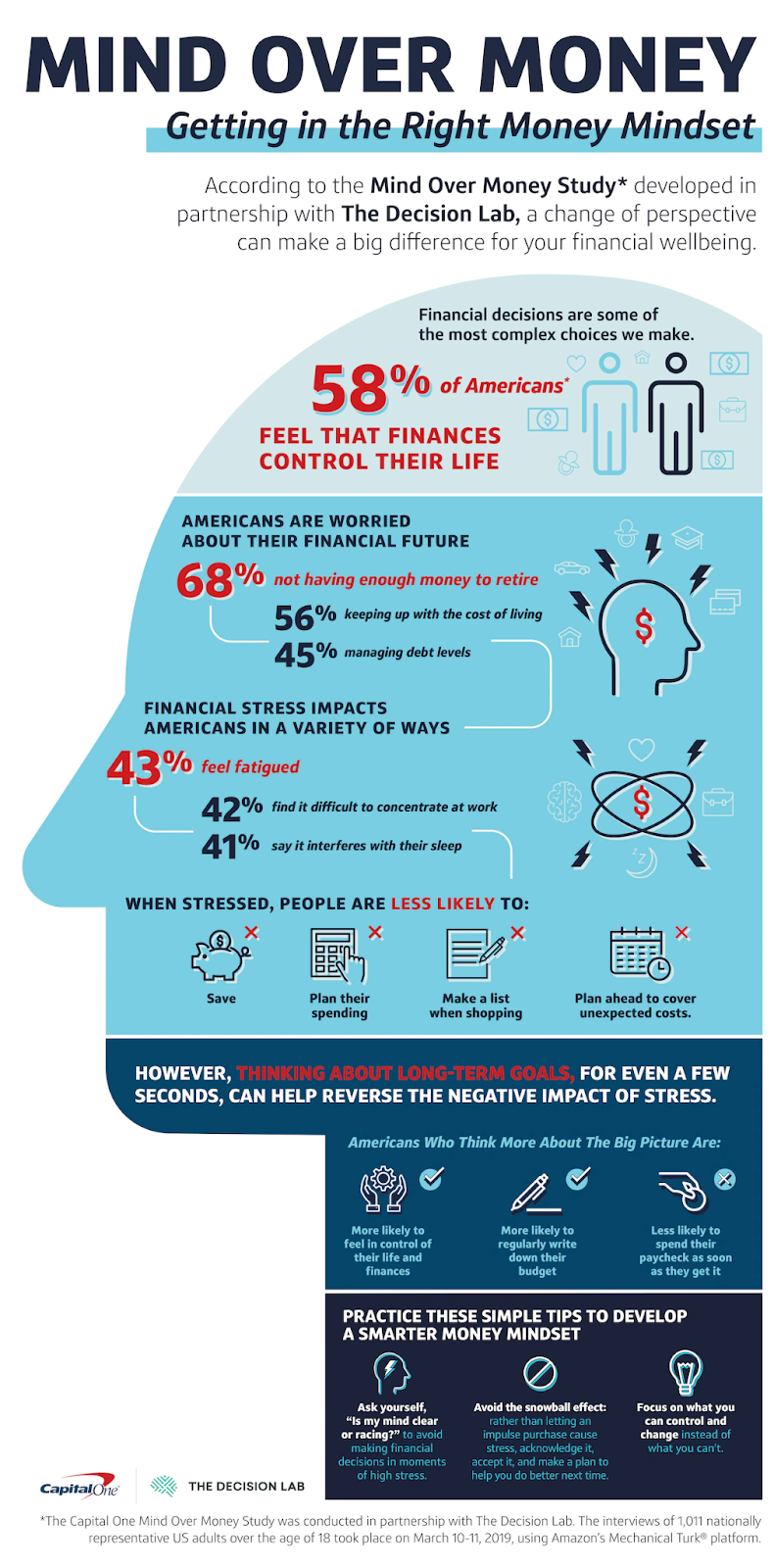

Money is the #1 source of stress for Americans,1 and it’s not hard to understand why. Financial decisions are some of the most complex choices we make: whenever we’re thinking of spending, we have to consider about the current balance in our bank account, the balance on our credit card, our upcoming expenses (groceries, gas, rent, student loan payments…), and to top it all off, our longer-term financial goals. It’s enough to make anyone’s head spin.

Given this complexity, it’s no wonder that when bills start to pile up, our instinct is often to stick our heads in the sand. But as many of us know all too well, financial stress tends to set off a vicious cycle of anxiety and avoidance: we can’t bear to think about our financial situation, so we ignore it for as long as possible, racking up more debt and getting even more stressed out in the process.

Money is supposed to serve us — not the other way around. The first step towards financial well-being2 is dispelling the anxiety that so often clouds our relationship with money, so that we can start to develop a more balanced mindset. We teamed up with Capital One to better understand how to break the cycle of financial stress, empowering consumers to take back control of their money. Our research was picked up by hundreds of outlets, including Forbes3 and Bloomberg.4

How financial stress compounds

We started by surveying more than one thousand American participants about their relationship with their money, and the effects that financial stress had on them. The results confirmed what we already suspected: 77% of respondents reported that they feel anxious about their financial situation, and 58% said that they felt like their finances controlled their lives. Stressed-out participants were more likely to spend their paycheck impulsively, and less likely to save, plan their spending, make shopping lists, or plan for unexpected events.

But the consequences of money stress went beyond the realm of finances. Because of financial anxiety, 43% said they felt tired all the time; 42% said they had trouble concentrating at work; and 41% said that worrying about money caused them to lose sleep.

The bigger picture

What can we do to help free people from this painful cycle? To get at this question, we designed an experiment — a randomized control trial (RCT),5 to be exact — to test

When we’re operating at a high level of construal, we think of things in terms of “big-picture,” abstract concepts. Meanwhile, low construal puts our focus on the “here and now.” In other words, construal is all about how much distance we have from our decisions.

Stress puts us in low-construal mode: it activates our fight-or-flight response, shifting our attention to our immediate environment. We evolved this instinct because it helps us respond to threats. Unfortunately, it also blinds us to the wider context in which we’re making decisions, which isn’t great for our wallets.

Luckily, construal levels aren’t static. Through a simple intervention, we were able to shift the mindsets of our participants towards seeing the bigger picture. When we asked participants to reflect on why they wanted to save money, we saw a 15% reduction in the effects of stress on financial decisions: people were more likely to feel in control of their finances, more likely to regularly write down their budget, and less likely to impulsively spend their paychecks.

Small nudges, big impact

Financial stress is a problem that resonates widely across our society. In our study, we found that the negative effects of financial stress were constant even when we controlled for household income and FICO scores. In other words, even though it goes without saying that having less money is more stressful than having more money, in many cases, the anxiety caused by finance is strongly related to our mindset.

Our findings show that simple interventions that help people see the “zoom out” before making financial choices can go a long way in supporting financial well-being. Here are a few simple strategies6 for stepping back from financial anxiety:

1. Make important decisions under low stress

You may not be able to control when you feel stressed, but you can control when and how you make decisions about spending money. Try scheduling big decisions for times when you’re likely to feel more relaxed, and find a calm environment to think things over.

2. Focus on values over features

In a world of nearly infinite options, it’s easy to get bogged down in minute details and lose sight of the bigger picture. If you find yourself agonizing over which vacuum cleaner to buy or whether or not to splurge on a fancy stand mixer, ask yourself: “Is this in line with my long-term goals? How will this purchase affect my wider plans?”

3. Use goal-directed accounts

To embed your values into your financial planning, harness the power of mental accounting to your advantage. Open separate bank accounts dedicated to a particular goal — for example, a vacation fund — and save a set percentage of your monthly income in each.

4. Don’t punish yourself for past purchases

There’s no use beating yourself up over money that’s already spent. Rather than stressing out over every impulse purchase, accept that mistakes happen, and try to treat it as a learning experience. For instance, try going over the sequence of events that led you to this decision and consider what you could change in the future to decrease the likelihood it will happen again.

References

- Bethune, S. (2015). Money stress weighs on Americans’ health (No. 4). American Psychological Association. https://www.apa.org/monitor/2015/04/money-stress

- What is Financial Well-being and Why is it Important? (2021). Capital One. https://www.capitalone.com/about/newsroom/financial-well-being/

- Navarrete, A. (2020, January 31). Mind Over Money: How To Develop A Smarter Money Mindset. Forbes. https://www.forbes.com/sites/capitalone/2020/01/28/mind-over-money-how-to-develop-a-smarter-money-mindset/?sh=43942a9426bb

- Big-Picture Thinking May Improve Americans’ Financial Decision Making, Mitigate Effects of Stress According to New Study from C. (2020). Bloomberg. https://www.bloomberg.com/tosv2.html?vid=&uuid=c7495a2b-e8f5-11ec-8472-68596b4f7071&url=L3ByZXNzLXJlbGVhc2VzLzIwMjAtMDEtMjgvYmlnLXBpY3R1cmUtdGhpbmtpbmctbWF5LWltcHJvdmUtYW1lcmljYW5zLWZpbmFuY2lhbC1kZWNpc2lvbi1tYWtpbmctbWl0aWdhdGUtZWZmZWN0cy1vZi1zdHJlc3MtYWNjb3JkaW5nLXRvLW5ldy1zdHVkeS1mcm9tLWM=

- Krastev, S., Pilat, D., Martin, M., Montenegro, M., & Struck, B. (2020, January 16). Construal level as a mediator of stress-induced bias in financial decision making. https://doi.org/10.31234/osf.io/hr8nk

- Mind Over Money: Develop a Smarter Money Mindset. (2020, January 27). Capital One. https://www.capitalone.com/about/newsroom/2020-capitalone-mindovermoneystudytips/