Why do we think less about some purchases than others?

The

Mental Accounting

, explained.Bias

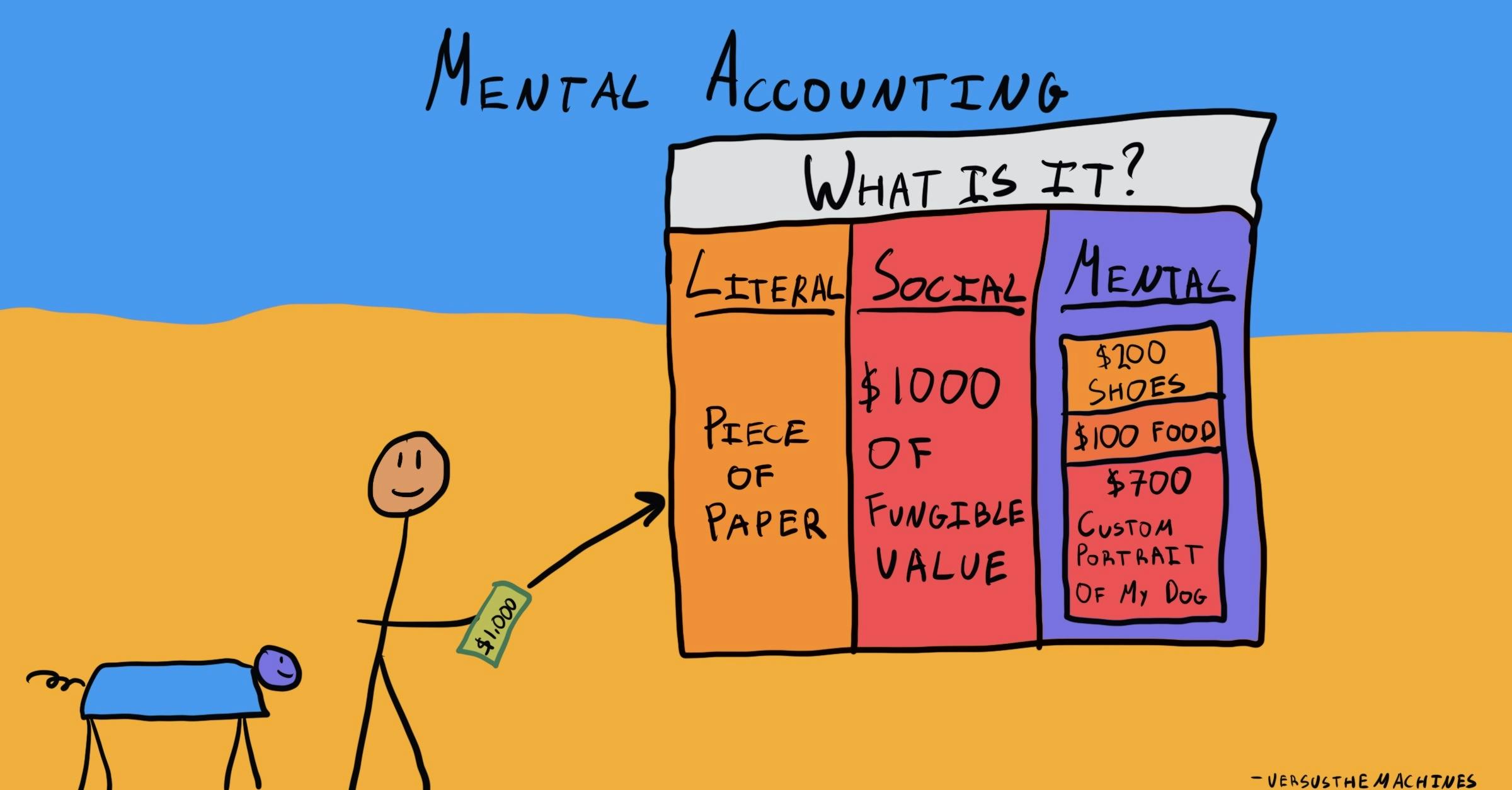

What is Mental Accounting?

Mental accounting, also known as mental accounting theory, explains how we tend to assign subjective value to our money, usually in ways that violate basic economic principles.1 Although money has consistent, objective value, the way we go about spending it is often subject to different rules, depending on how we earned the money, how we intend to use it, and how it makes us feel.