The behavioral biases behind our investments with Clare Flynn Levy

But when you start to do analysis at the aggregate level of every position you've ever held, and your job is to hold hundreds or thousands of these positions, you start to see, "Oh gosh, this is what it looks like for me when the price is going down and down and down, and I wait way too long." Then you can use data analytics to figure out what would've been the point historically, where you should have pulled the plug.

Listen to this episode

Intro

In this episode of the podcast, Brooke speaks with Clare Flynn Levy - CEO and Founder of Essentia Analytics, a company that uses behavioral data analytics to help professional investors make more skilled investment decisions. Drawing from her own experience as a fund manager, Clare shares her insights into the types of biases that influence investment decision making and the evolution of behavioural interventions that seek to address them. Some of the things discussed include:

- How investors can identify patterns in their decision-making and understand where things might be going wrong.

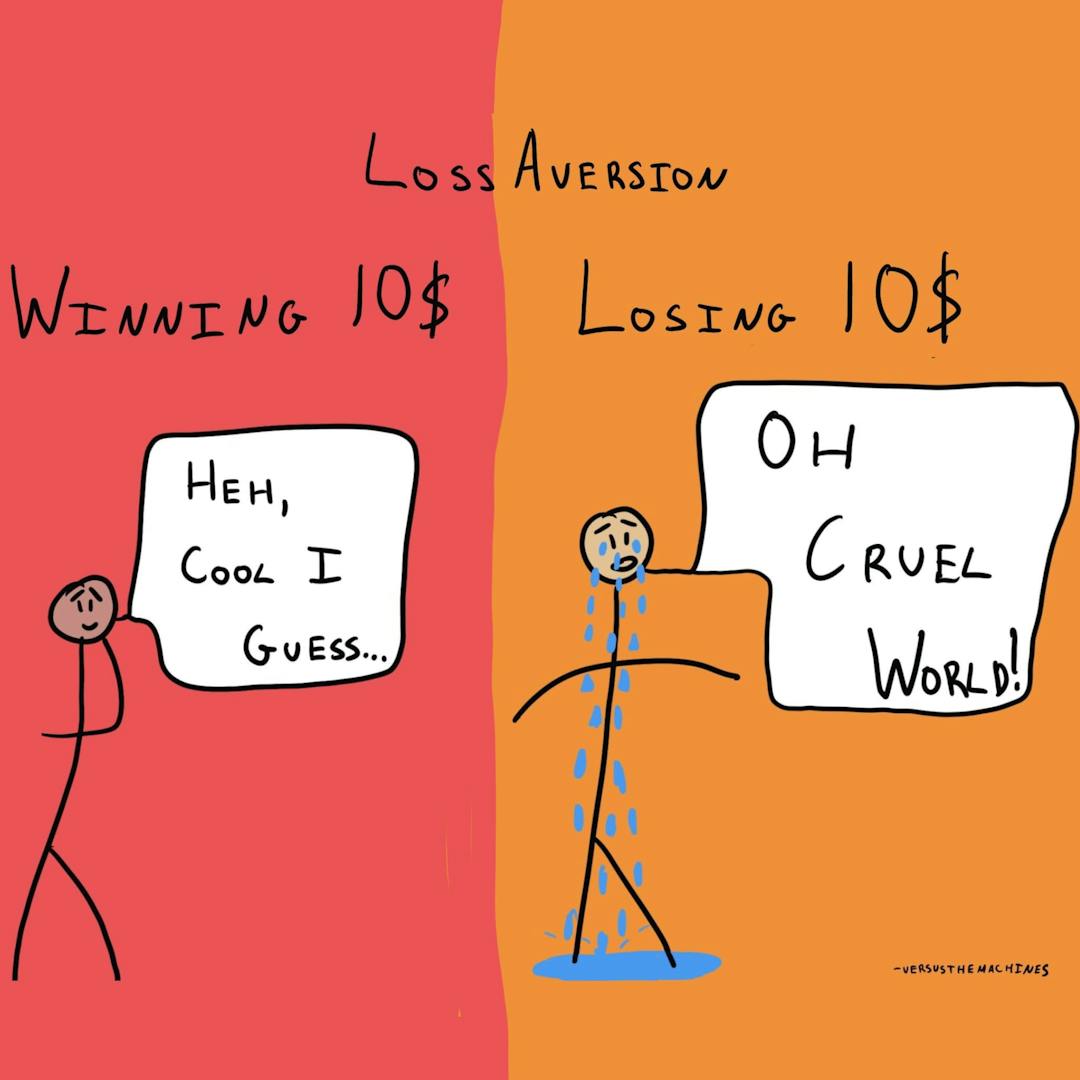

- Exit-timing and the role of loss aversion.

- The endowment effect, fear of missing out and other common behavioural patterns.

- How Clare and her team work to automate the questions investors should be asking themselves before each important decision.

- Strategies that investors can adopt to overcome the behavioural biases that might be hindering their performance - starting tomorrow