Alfred Marshall

Alfred Marshall and the Principles of Economics

Intro

Alfred Marshall was one of the most influential economists of the late 19th and early 20th centuries. His book, Principles of Economics, was published in 1890 and quickly became a dominant economic and mathematical textbook in England. It is still used today in classrooms around the world.1 Marshall is viewed as the founder of the neoclassical school of thought in economics and was the first to introduce many now-standard principles of the field. Neoclassical economists were interested in how agents, consumers, and producers maximize the function of scarce resources in a given market.2 Marshall’s articulation of the relationship between supply and demand was central to neoclassical economist foundations and his concepts endure today in many economic models and theories.1

Alfred Marshall originally studied as a mathematician but understood that economic principles were vital to everyone’s livelihood and that it was important that it could be understood by the general population.3 Alfred Marshall sought to bring economics to the layman so that everyone could better understand their decision-making habits. In Principles of Economics, he was careful to always try and contextualize economic principles through real-life examples to ground his abstract theories. He wanted people to understand how economics applied to their daily habits.3

Alfred Marshall was a jack-of-all-trades. He studied mathematics, philosophy and ethics, and metaphysics, although his most notable contributions to our times were in the field of economics.4 He specifically was interested in microeconomics. He studied the way individuals make decisions, which is crucial for applied science. He not only had a brilliant mind but was a brilliant teacher and changed the way that economics was taught by appealing to a more general population. Marshall wanted to humanize economics because he believed that every man sought his own, or at least his children’s best interest.5 Two of his most important contributions to economics include introducing time into the conversation about supply and demand and the idea of consumer surplus.

He understood the ways in which people derived from rational economic principles:

the laws of economics are to be compared by the laws of the tides, rather than with the simple and exact law of gravitation. For the actions of men are so various and uncertain, that the best statement of tendencies, which we can make in a science of human conduct, must needs be inexact and faulty.

On their shoulders

For millennia, great thinkers and scholars have been working to understand the quirks of the human mind. Today, we’re privileged to put their insights to work, helping organizations to reduce bias and create better outcomes.

Founding Neoclassical Thought & Behavioral Science

Prior to Marshall’s time, classical economics focused on wealth and was more interested in macroeconomics, which examines the market through the wealth of a nation as a whole. Classical economics understood production costs as the most important factor in determining the price of a product because it assumed that people were rational consumers.

Alternatively, neoclassical thought that a consumer’s perceived value of a product determined its market price. It assumed that the utility of a product matters more in purchasing decisions than how much it costs to produce and that people would buy something for a higher price than production cost if they believed they would derive greater utility from it. The difference between the cost of production and the actual market price was called economic surplus for neoclassical economists.7 Neoclassical thought was better able to account for the ways in which humans make decisions that deviate from rational logic; in other words, it leaned more towards behavioral science than pure math.

Albert Marshall may have founded the Cambridge School of Neoclassicism but he did not wholly write off the benefits of classical economics.4 Marshall left room for more than one factor influencing price and that different schools of economic thought could be useful for explaining different periods. For example, he believed that perceived utility may have a greater impact on price in the short-term but the cost of production may have a greater influence on the price in the long-term.3

Marshall was attempting to pair a mathematical system with the reality that consumers are not always purely rational and can be influenced by their beliefs. His book, the Principles of Economics, later became the guide that brought British neoclassicism to the rest of the world.4

The demand that Marshall supplied

It was in the Principle of Economics that the economic world first encountered Marshall’s supply and demand graph that emphasized his theory of value. As discussed, Alfred Marshall sought to join together the influences of cost production and consumer utility. His supply and demand graph demonstrated that the market price of a good, and the output of a good, are dependent on both supply and demand.8 Value was therefore determined by supply and demand.

Marshall claimed that the supply and demand were like two blades of a pair of scissors:

“We might as reasonably dispute, whether it is the upper or under blade of a pair of scissors that cuts a piece of paper, as whether value is governed by utility or cost of production. It is true that when one blade is held still, and the cutting is effected by moving the other, we may say with careless brevity that cutting is done by the second; but the statement is not strictly accurate, and is to be excused only so long as it claims to be merely a popular and not a strictly scientific account of what happens.” 9

What this meant is that in different time periods, either the supply or demand may be the fixed blade, which means that market price is the price ruling at a particular period but not for all of eternity. Marshall understood that depending on the time-line of a product’s launch, supply and demand would shift in different ways, meaning that price could be influenced by either.

Essentially, Alfred Marshall’s understanding of the supply and demand curves incorporated the idea of time into how value is determined. This revolutionized the economic understanding of market price and these graphs are still used today to calculate and predict shifts in the market.

Consumer Surplus

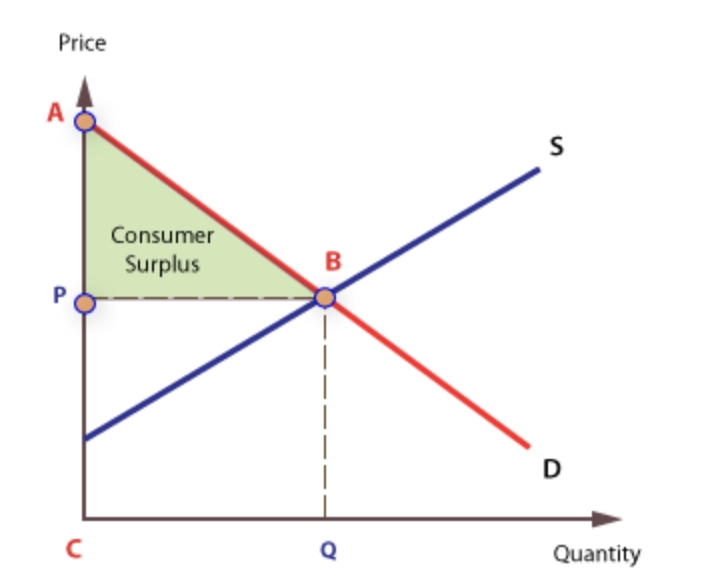

Another important contribution that Alfred Marshall made to the field of economics was a concept he termed consumer surplus. In the Principle of Economics, Marshall said that “the excess of price which he would be willing to pay rather than go without the thing, over that which he actually does pay, is the economic measure of this surplus satisfaction.” 9

What this meant is that often, many people would actually be willing to pay more than the market price for a good because they perceive a high utility that they derive from the product, as shown by the graph be

These consumers, therefore, enjoy an extra benefit, which is demonstrated through the shaded region in the graph to the left. An example of consumer surplus would be to imagine that you wanted a new hockey stick and were willing to pay $80 for it. The actual market price is $65, so the consumer surplus is $15.

While today, this might seem like a relatively understood concept, in Marshall’s time, economic models hadn’t properly taken into account the different beliefs, preferences, and budgets of different people. Instead, they believed all consumers would behave the same. As many cognitive biases demonstrate, these perfect economic models often do not fully account for the way that the world works.

Marshall used his ideas about consumer surplus to discuss market welfare, which is the study of how the allocation of economic goods and resources determine the overall well-being of society.10 He was therefore able to analyze how taxation and price shifts would affect the overall wellbeing of consumers.3 It is clear that from principles like consumer surplus, Marshall was interested in democratizing economics and felt that economics could be approached with ethical values in mind.

Historical Background

Alfred Marshall was born in 1832 in London, into a middle-class family. His father, William Marshall, worked as a clerk at the Bank of England, which may have sparked Alfred’s interest in money and numbers.4 Alfred showed great promise as a young mathematician in high school and planned to go to the University of Cambridge to become a member of the Anglican church.5 While at Cambridge, Marshall changed his mind and graduated in mathematics. Still unsure of what was the best next step, Alfred Marshall spent the next few years changing disciplines, moving from physics to psychology, to ethics, and finally to economics. He viewed economics as a practical means of implementing ethics.5

In 1868, Alfred Marshall became a professor of political economy at the University of Cambridge.3 It was through teaching this class that almost ten years later, Marshall met his wife, Mary Paley, who was a student in his class. However, Cambridge had a strict policy about professors and students fraternizing, which caused Marshall to have to leave his post.3 He became principal and professor at Bristol University College but because his administrative duties took up too much of his time, Mary was left to take on most of the responsibilities of the class. Mary Paley also had a brilliant mind and affinity for economics and is thought to have helped Alfred write his books.11 Marshall eventually returned to Cambridge to teach after the death of a colleague.3 In this final appointment, Marshall fought to create a new tripos, which is the final honors examination at Cambridge for economics. He succeeded in 1903 and retired in 1908.4

Alfred Marshall started writing his masterpiece, the Principles of Economics, in 1881, a few years before he returned to Cambridge. He planned for his work to develop into a two-volume compilation about all things economics-related. The published book in 1890 is actually only the first volume. The second volume, which addressed different economic principles such as foreign trade and tax, was never published.3 Marshall may have been a bit of a perfectionist and took on too big a task, causing him to feel as though the second volume was never quite finished. Marshall later published Industry and Trade in 1919 and Money, Credit, and Commerce, but neither of these received nearly as much critical acclaim as his first publication.3 Alfred Marshall died peacefully in his home in 1924, at the age of 81.4

Marshall’s wisdom

Alfred Marshall approached economics with an ethical mindset, wanting economics to help explore the ways in which market welfare could be improved upon. He once stated, “the most valuable of all capital is that invested in human beings.”6 He had hope that economics did not just have to be about the wealthy: “the hope that poverty and ignorance may gradually be extinguished, derives indeed much support from the steady progress of the working class during the nineteenth century”,12 perhaps because he himself came from the middle class.

He wanted economics to attend more closely to the reality of the market, instead of higher-order logic. He said, “there has always been a temptation to classify economic goods in clearly defined groups, about which a number of short and sharp propositions could be made, to gratify at once the student’s desire for logical precision, and the popular liking for dogmas that have the air of being profound and are yet easily handled. But great mischief seems to have been done by yielding to this temptation and drawing broad artificial lines of division where Nature has made none. The more simple and absolute an economic doctrine is, the greater will be the confusion which it brings into attempts to apply economic doctrines to practice if the dividing lines to which it refers cannot be found in real life.” 6

His desire also influenced the way that he understood economic terms and concepts; not as having a fixed meaning but being meaningful in relation to particular contexts. He viewed it akin to general language, where “in common use almost every word has many shades of meaning, and therefore needs to be interpreted by the context.” 13 This line of thinking is similar to a belief held by Ludwig Wittgenstein, a famous philosopher, that language must be discussed and understood in relation to its use.

Where can we learn more?

If you are intrigued by the mention of Alfred Marshall’s Principles of Economics, you may want to give the book a read. Although the book was published over 100 years ago, the principles discussed in the book are still very relevant to modern economics, and it is often used as a kind of textbook in economics classrooms. It can be accessed for free through the Library of Economics and Liberty.

However, the Principles of Economics is almost a 700-page book, meaning that unless you are deeply interested in economics, it may not be the right fit for you. You may be more interested in listening to episode two of season three of Economics in Ten in which the two hosts, Pete and Gav, take their audience through Alfred Marshall’s notable contributions to economics.14

If you’re interested to see how Alfred Marshall’s theories stand against contemporary economic issues, then you might want to read Neil Hart’s Alfred Marshall and Modern Economics. The book traces Marshall’s legacy through its relevance to modern economic analysis.

If you’re more interested in a less refined version of Alfred Marshall’s economic theories, you may want to read The Correspondence of Alfred Marshall, Economist. This book compiles some of Marshall’s unpublished economic theories into a three-volume work. In reading through the letters he wrote to his colleagues, we can gain a better understanding of who Marshall was as a person, by getting insight not only into his economic views but also his political and social views.

References

- The Editors of Encyclopaedia Britannica. (1998, July 20). Alfred Marshall. Encyclopedia Britannica. https://www.britannica.com/biography/Alfred-Marshall

- Policonomics. (2012, March 29). Neoclassical School of economics. https://policonomics.com/neoclassical-school-of-economics/

- New World Encyclopedia. (n.d.). Alfred Marshall. Retrieved October 6, 2020, from https://www.newworldencyclopedia.org/entry/Alfred_Marshall

- History of Economic Thought. (n.d.). Alfred Marshall, 1842-1924. Retrieved October 6, 2020, from https://www.hetwebsite.net/het/profiles/marshall.htm

- Your Dictionary. (n.d.). Alfred Marshall Facts. Retrieved October 6, 2020, from https://biography.yourdictionary.com/alfred-marshall

- Goodreads. (n.d.). Alfred Marshall Quotes. Retrieved October 6, 2020, from https://www.goodreads.com/author/quotes/368788.Alfred_Marshall

- Kenton, W. (2020, September 24). Neoclassical Economics. Investopedia. https://www.investopedia.com/terms/n/neoclassical.asp

- The Library of Economics and Liberty. (n.d.). Alfred Marshall. Retrieved October 6, 2020, from https://www.econlib.org/library/Enc/bios/Marshall.html

- Shailesh, K. (2016, May 23). Top 14 contributions of Alfred Marshall to economics. Economics Discussion. https://www.economicsdiscussion.net/economics-2/alfred-marshall/top-14-contributions-of-alfred-marshall-to-economics/21044

- Chappelow, J. (2019, October 11). Welfare Economics. Investopedia. https://www.investopedia.com/terms/w/welfare_economics

- SunSigns. (2018, February 21). Alfred Marshall. https://www.sunsigns.org/famousbirthdays/d/profile/alfred-marshall/

- Brainy Quote. (n.d.). Alfred Marshall Quotes. Retrieved October 6, 2020, from https://www.brainyquote.com/authors/alfred-marshall-quotes

- The Famous Quotes. (n.d.). 19 Interesting Quotes By Alfred Marshall For The Scholarly. Retrieved October 6, 2020, from https://quotes.thefamouspeople.com/alfred-marshall-3571.php

- Apple Podcasts. (n.d.). Apple Podcasts Preview. Retrieved October 6, 2020, from https://podcasts.apple.com/us/podcast/season-3-episode-2-alfred-marshall/id1450116373?i=1000480128258

About the Author

The Decision Lab

The Decision Lab is a Canadian think-tank dedicated to democratizing behavioral science through research and analysis. We apply behavioral science to create social good in the public and private sectors.